Audit quality

Public audit plays a key role in providing assurance that public money is well managed and in providing independent and objective evidence on the performance of public bodies. That assurance is important for the public and decision-makers and will become even more important as Scotland assumes greater fiscal autonomy within the UK. We want the public interest, trust and confidence to be at the heart of Audit Scotland’s work.

How public audit in Scotland works

Public audit in Scotland is informed by the priorities of the Auditor General and the Accounts Commission. Our document Public audit in Scotland sets out the shape, principles and themes of public audit. And our Corporate plan sets out how public audit is delivered.

Public audit in Scotland

Public audit in Scotland Corporate Plan

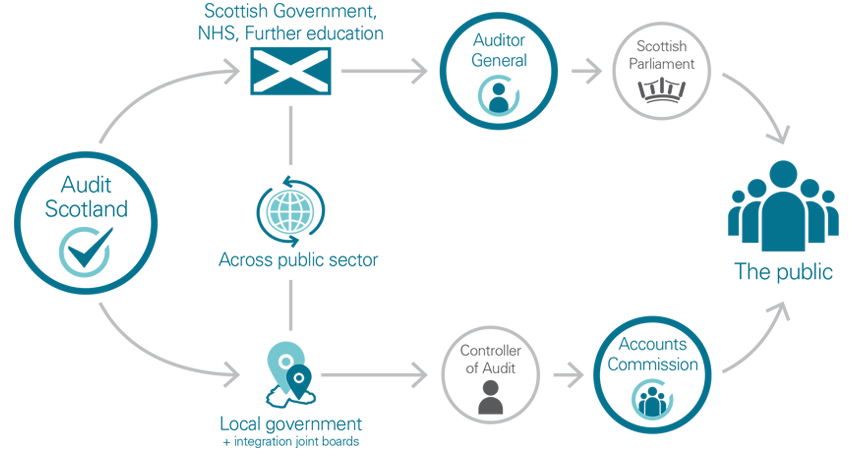

Corporate PlanScottish public-sector bodies do not appoint their own auditors. The Auditor General appoints auditors to all Scottish Government, NHS, further education and other central government bodies. The Accounts Commission appoints auditors to all councils and local government bodies.

Who we are

Audit Scotland audits bodies across the public sector:

Scottish Government, NHS and further education are audited through the Auditor General who reports findings to the Scottish Parliament

Local government is audited through the Controller of Audit, who reports to the Accounts Commission

Both the Parliament and the Accounts Commission are accountable to the public

The independent appointment of auditors is a strength of public audit and is an important safeguard that helps to ensure that the auditor is free from any potential or perceived conflict of interest or other pressure which may compromise their judgement. More information can be found on our audit appointments web page.

Audit Scotland's commitment to audit quality

We are committed to the consistent delivery of high-quality public audits as that is the foundation for building consistency and confidence across all audit work. High-quality audits provide assurance, add value and can support public bodies to achieve their objectives. As commissioners of public audit, the Auditor General and the Commission require all annual audits delivered by appointed auditors, as well as the performance audits carried out on their behalf, to be performed to the highest quality. They therefore require Audit Scotland to provide independent assurance on the quality of these audits.

The Audit Quality in Audit Scotland report explains the arrangements for providing assurance on the delivery of high-quality annual audits and performance audits of public bodies in Scotland. There are two sections in Audit Scotland that support these arrangements: Audit Quality and Appointments, and the Innovation and Quality (I&Q) business group.

Audit Quality and Appointments team

This team is independent of staff working on audits. They produced and maintain the Audit Quality Framework, which applies to all audit work and providers, and report on audit quality to the Auditor General, Accounts Commission and the public.

Audit Quality Framework

The framework combines the highest professional and ethical standards with strong and comprehensive arrangements for:

- internal quality reviews

- reporting on quality to the Audit Committee, the Auditor General, the Accounts Commission and to the public

- external quality reviews commissioned from the Institute of Chartered Accountants of Scotland (ICAS). They carry out independent reviews covering all aspects of our audit work and providers, including financial audit, best value audit and performance audit.

Quality of public audit in Scotland annual report

The results of the work under the Audit Quality Framework are published in June each year.

Innovation and quality

Our I&Q business group was established to drive continuous improvement in audit quality by leading organisational transformation and development to ensure that Audit Scotland’s audit work is innovative and at the forefront of the audit profession. I&Q seeks to ensure that Audit Scotland:

- deploys world-class, cutting-edge audit methodologies;

- embed a culture of innovation and continuous improvement;

- develops and retains staff, and attracts high calibre new recruits; and

- innovates to make audit delivery as efficient and impactful as possible, taking full advantage of new technologies.

I&Q comprises four complementary functions that work in a collaborative manner to achieve the group's objectives. These are: internal quality monitoring activities; professional support, guidance and learning (see the technical guidance page); digital audit and data analytics; and organisational improvement and transformation. In addition, the Executive Director of I&Q is Audit Scotland’s Ethics Partner.

Transparency Report

Each year, we publish a report which pulls together a number of strands related to the quality of audits delivered by Audit Scotland. The most recent report covers activities during the 2022/23 financial year and:

- explains the role of Audit Scotland in delivering high quality audits

- sets out the results of internal and external quality reviews

- provides information on meeting audit completion dates

- includes the results of a survey on how well audit colleagues feel they were supported in delivering high-quality audits

- gives examples of where audits have added value.